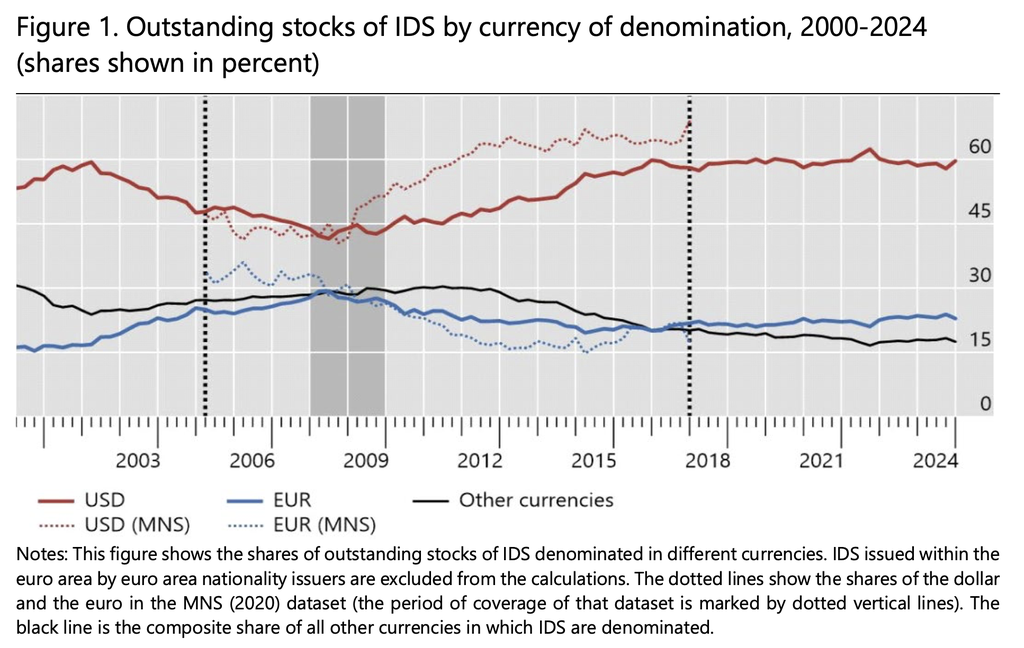

The role of the U.S. dollar in global bond markets has waxed and waned periodically over the past 60 years, with no clear long-term trend toward increasing dollar dominance or de-dollarization, according to a new Federal Reserve discussion paper.

Using the Bank for International Settlements' (BIS) international bond database, the authors identify three distinct “waves of dollarization” since the 1960s and show that changes in currency use have followed a cyclical pattern rather than a steady structural change in global finance.

“There is no monotonous dollarization or de-dollarization trend. Instead, the dollar share shows a wavy pattern,” the paper said.

According to the report, the most recent wave emerged after the 2008 global financial crisis, when the dollar regained market share in international debt issuance, returning to levels seen before the surge in euro-denominated debt issuance in the early 2000s.

Proportion of international debt issued by currency, 2000-2024. sauce: federal reserve system

The study also found that as of 2024, emerging market issuers will still rely primarily on dollar-denominated debt, which accounts for about 80% of international debt issuance, while China's efforts to internationalize its currency, the renminbi, which began in 2010, have yielded only modest gains.

“The dollar's pre-eminence rests on a weak foundation, but in the absence of viable alternatives, the dollar's primacy remains unchallenged,” the report said.

Related: Intuit to use Circle's stablecoin for financial platform

Stablecoins back U.S. Treasuries

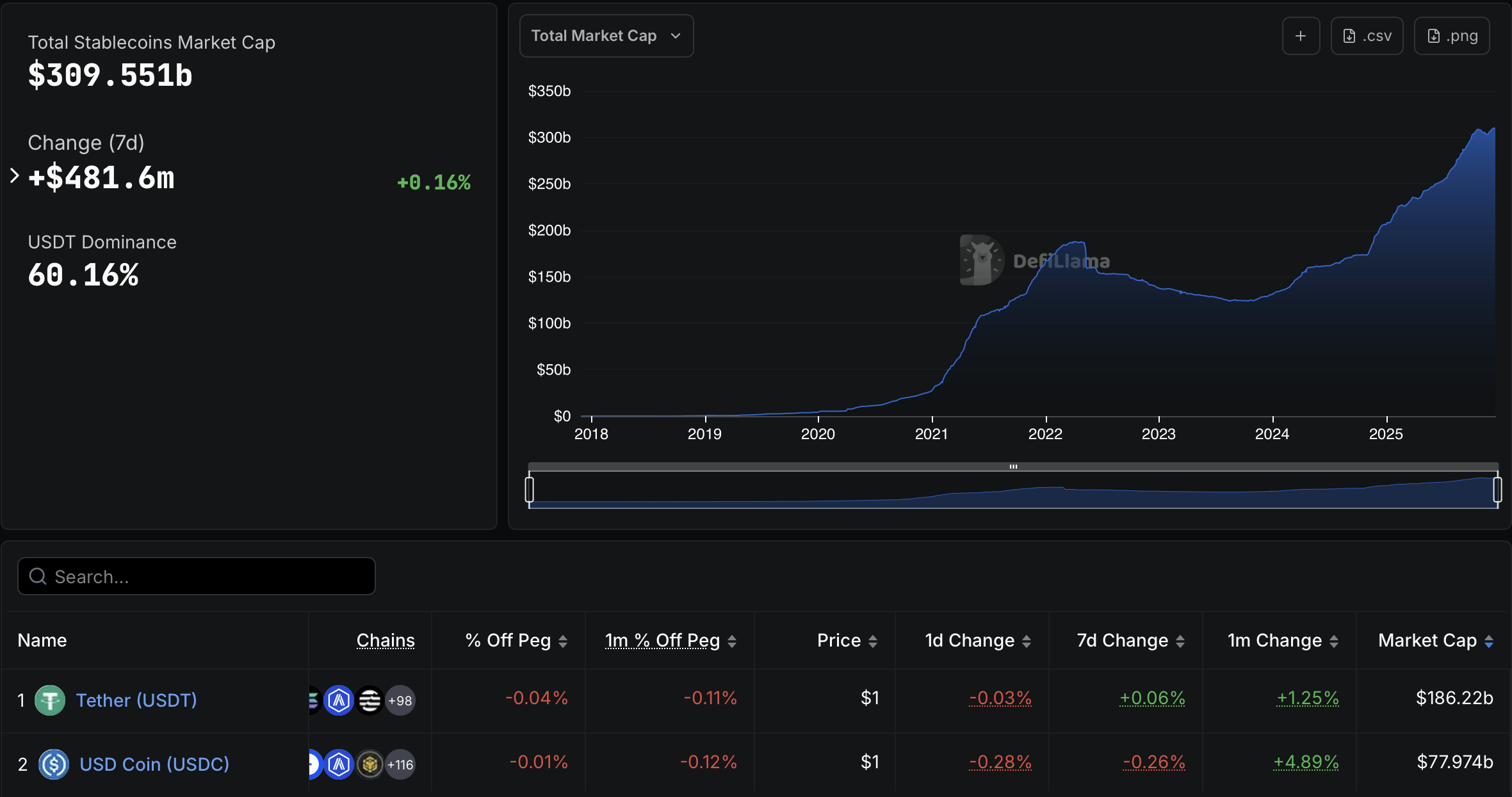

The global stablecoin market has expanded rapidly over the past year, growing from $205.5 billion in December 2024 to approximately $309.6 billion, according to data from DefiLlama.

Most of that growth has been concentrated in USD-pegged tokens, with Tether’s USDt (USDT) and Circle’s USDC (USDC) together accounting for about 85% of the total stablecoin supply, or about $264 billion of the market at the time of writing.

Stablecoin market capitalization. sauce: Defilama

As dollar-pegged stablecoins have expanded, issuers have become significant holders of short-term U.S. Treasuries.

Tether said in its second quarter 2025 reserves report that its exposure to U.S. Treasuries exceeded $127 billion, including $105.5 billion in direct holdings and $21.3 billion in indirect holdings. This level of Treasury holdings makes Tether one of the largest holders of U.S. government debt, the company said.

USDC is also heavily supported by U.S. government debt instruments, including $49.7 billion in overnight reverse repos and $18.5 billion in short-term Treasury bills, according to Circle's latest transparency report (dated December 15).

Preliminary composition of the circle. December 15, 2025. source: circle

The U.S. government sees dollar-pegged stablecoins as a way to strengthen the dollar's role as the world's reserve currency and is supporting their growth through legislation, according to a July report from digital asset bank Sygnum.

Other countries are also paying attention. Italian Economy and Finance Minister Giancarlo Giorgetti warned in April that U.S. policies supporting dollar-backed stablecoins posed a greater long-term risk to Europe's financial system than trade tariffs, saying they could undermine the euro's role in cross-border payments.

In December, a group of 10 European banks announced plans to launch a euro-pegged stablecoin in the second half of 2026.

magazine: Introducing on-chain crypto detectives who fight crime better than the police